The first half of 2021 has proven very favorable to financial markets. This was due to a convergence of three important factors:

- low interest rates

- defendable valuation levels

- ongoing recovery from the covid crisis

The first factor is likely to remain for a long period of time no matter the talk about increases in interest rates. Since the financial crisis of 2008, rates globally have only gone down and remained low except for brief increases. It will be most challenging for any central banks to increase rates markedly in the foreseeable future for two reasons. First, the level of sovereign and corporate indebtness is at record levels and the only reason this has proven sustainable so far is because of low rates. Increasing them would push many firms and governments into financial hardship. Secondly, a significant increase in rates could lead to major falls in financial markets. For thirteen years now, central banks have done everything to prevent major drops in the financial assets as they would adversely affect both financial institutions and individuals.

In recent months, inflation has increased markedly worldwide and in the US in particular. It is up for debate whether this is, as the Fed is telling, a temporary increase due to supply disruptions following the covid crisis or a more lasting change in trend. The return of inflation has been announced since the accommodating monetary policies started in 2008 and despite all the “money printing” it has not happened. However, there are reasons why this time might be different. Inflating sovereign and corporate debt away through might prove the most convenient way for governments to reduce debt. It is therefore essential for prudent investors to address inflation risks.

With markets at historical highs and valuation levels elevated by historic standards it may look like the second factor is increasingly under risk. However, simply comparing the current situation to historic valuation levels, as some veteran investors do, is shortsighted. This is because the first factor mentioned above, the interest rates, are at unprecedented historic lows. With government bonds yielding about 0% and inflation picking up, an equity or a real estate investments yielding 2-3% and offering some inflation protection might be attractive. Based on next-year’s earnings forecasts the S&P 500 is currently trading at a P/E of about 20 times earnings equivalent to a 5% yield. This means that there is still considerable upside potential left.

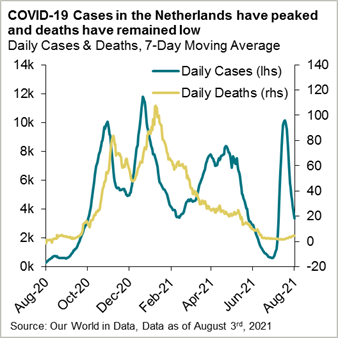

The third factor, the covid risk, is certainly the most significant and unpredictable. The delta variant is currently raising lot of concern and media attention in Israel and globally. While we would guard against the pitfall of trying to make predictions, a certain number of recent developments are very significant and encouraging. India, where delta started, is no longer in the headlines. More importantly, the UK which on July 19th lifted basically all the covid restrictions is so far doing well. Cases peaked but the number of deaths remained relatively low suggesting that due to vaccines and, possibly other parameters too, the lethality of covid diminished. Similarly, the Netherlands also experienced a delta wave with a surge in cases but a relatively low number of deaths as illustrated in the graph below. That bodes well for the rest of the world where the delta wave is still growing.

In summary, the outlook for the second half of the year and possibly beyond looks positive. Despite the record highs, investors able and willing to take into account volatility can maintain a risk-on approach with a higher than average stock market exposure. Investors looking for stability should continue to focus on a higher allocation to uncorrelated returns. While correlation is of course desirable when markets go up, when dramatic developments happen, almost always unexpectedly, the uncorrelated portfolios are the ones holding their own.

Orit Raviv Swery Ilan WeilFounder & CEO Chief Investment Officer